Monster (NASDAQ: MNST)

Monster (NASDAQ: MNST) is set to report its Q3 2020 earnings today after the bell, and if history is any guide, shares have a 75% chance of increasing tomorrow post-earnings (it has happened six of the past eight times).

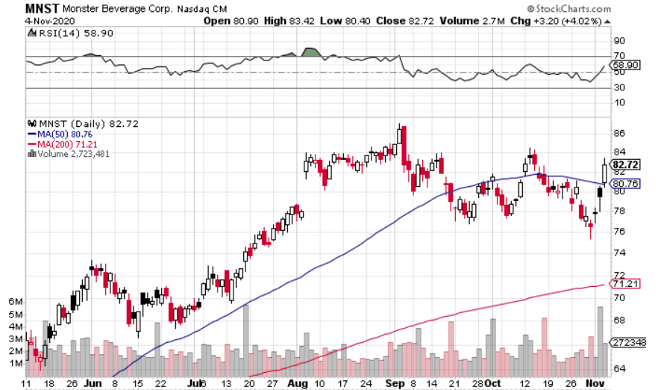

Monster shares have been range-bound since gapping up post-Q2-earnings, but they’re already up 8% this week.

Here are three reasons why I think Monster will, again, jump post-earnings:

1. International Expansion is Still on Track

Monster posted a strong Q2 overall, but headwinds abroad led to a contraction in international sales. Net sales to customers outside the US were $328.3 million, down from $343.3 million in Q2 2019. That performance compared unfavorably to Q1 2020, when international sales increased more than 25% yoy.

Monster pointed to currency headwinds and weakness in EMEA countries – many of which experienced lockdowns. Monster did, however, outperform its competitors in many of these countries, growing its market share in Denmark, Great Britain, Greece, Norway, Poland, Republic of Ireland, South Africa, Spain and Sweden.

Asia was a different (and better) story with Japan increasing 41.8% yoy, South Korea up 46.9% yoy, and China soaring 66.9% yoy.

Even if the EMEA numbers improved a bit in Q3, Monster is going to face an uphill battle in Q4 with a lot of European countries instituting new lockdowns. That could lead to cautious Q4 guidance. But if there is continued strength in Asia – which I think there will be – I think that will be enough to keep investors happy.

2. Convenience/Gas Channel Trending in the Right Direction

The convenience/gas channel is Monster’s largest channel. Back in June, I noted that this channel was a drag on revenue in the early stages of the pandemic. But I also pointed out that the decrease seemed short-term in nature.

Well, even I wasn’t expecting convenience/gas to rebound so quickly; sales were soft early in Q2, but “improved sequentially throughout the quarter.”

That improvement appears to have continued into Q3. On the Q2 earnings call, Monster CEO Rodney Cyril Sacks said, “According to Nielsen, for the four weeks ended July 18, 2020, sales in the convenience/gas channel, including energy shots in dollars increased 9.2% over the same period the previous year.”

3. Monster May Launch Hard Seltzer in 2021

The key word here is “may.” We talked about this back in August, ahead of the Q2 earnings release. But we cautioned that 2021 is just speculation at this point. Sacks was asked about Monster’s hard seltzer plans in the Q2 call; he acknowledged the speculation and said Monster is “analyzing it,” but didn’t offer anything definitive.

Nobody knows whether Monster will roll out any definitive plans in its Q3 call, but the way I see it, an announcement could push shares higher. On the other hand, I think if there’s a lack of commitment, investors will shrug it off.

But even if no announcement is made today, the potential for a hard seltzer launch sometime in the next year has me really excited. The hard seltzer market is on fire, and I’d like Monster’s chances of getting a piece of the pie – despite growing competition. Granted, I’d be shocked if a Monster hard seltzer can overtake White Claw or Truly. But even picking up, say, 5-10% market share would be a big win.

Risk/Reward is Attractive Ahead of Earnings

I’m not expecting any big upside surprises when it comes to #s 1 & 2, but I think the numbers/outlook will be strong enough to satisfy investors.

I could see a small post-earnings increase coming to fruition even if there is no hard seltzer announcement. But if there is a hard seltzer announcement, investors will salivate at the possibilities, and potentially send shares a lot higher.

Bottom line, the risk/reward on Monster is attractive ahead of earnings, and you should consider getting in.

Companies in This Article: