Convenience retail products supplier

Core-Mark Holding Company (NASDAQ: CORE) shares are trading back to its pre-COVID levels and underperforming the benchmark

S&P 500 index (NYSEARCA: SPY). The distributor of consumer packaged products supplies food and non-food products ranging from sandwiches and juices to cigarettes and

beauty care products to over 42,000 locations from 32 distribution centers spanning the U.S. and Canada. The Company has been a pandemic benefactor as essential business customers experienced a surge of demand for consumer packaged products. As

commuters get back on the road,

convenience stores see more traffic and Core-Mark gains. With the restart initiative underway, shares should see a multiple expansion as businesses open back up. Prudent investors looking for a dual narrative play in the economic recovery from the distribution side should consider monitoring Core-Mark for opportunistic pullback levels.

Q2 FY 2020 Earnings Release

On Aug. 6, 2020, Core-Mark released its fiscal second-quarter 2020 results for the quarter ending June 2020. The Company reported an earnings-per-share (EPS) profit of $0.38 excluding non-recurring items versus consensus analyst estimates for a profit of $0.31, beating estimates by $0.07. Revenues fell (-1.7%) year-over-year (YoY) to $4.26 billion beating analyst estimates of $4.09 billion. The Company experienced unprecedented volume compression in the quarter but was flexible and assertive enough to adapt reducing operating expenses by nearly $5 million YoY. The Company estimates approximately $2 million to $4 million in permanent cost reductions can be sustained in a “more normal sales and margin environment.” Core-Mark ended the quarter with $108 million cash and $494 million revolver available.

Conference Call Takeaways

Core-Mark CFO, Scott McPherson, provided color on the quarter during the Q2 2020 earnings conference call. Convenience store (C-store) trips as an industry were down (-10%) to (-15%) for the quarter but rebound from the pandemic lows of (-25%) to (-30%) at the beginning for Q2. This was due to stay-at-home mandates that took cars off the roads. The steep drop in C-store trips were offset buy the increase in average size of the purchase basket rising 15% to 20% per trip. Neilson (NASDAQ: NLSN) data indicated that C-store volume were up 2% to 5% for the quarter. However, the bulk of those gains came from cigarette and alcohol sales overshadowing the decline in prepared foods, snack and alternative nicotine products. This trend matches the Company’s own metrics with total sales decline of (-1.7%) reflecting 2% growth in cigarette sales while non-cigarette sales declined (-9%) YoY.

Growth Driver Programs

Core-Mark relaunched and rolled out many programs to accommodate end-user demand to drive growth. The Company relaunched its SmartStock program “which pairs merchandising resources to world-class management.” The Grab, Heat and Go program was relaunched to bolster hot food items for consumers on-the-go. They also rolled out the Personal Protective Equipment Program as a turnkey solution for C-stores providing a wide selection of gloves, masks, sanitizers and cleaning supplies to meet consumer demands in the pandemic. The Company plans to launched its private-label program Core-Mark Curated, which “is focused on bringing new, innovative products to the convenience and retail industry.”

Full-Year Guidance Forecast

Core-Mark had previously pulled full-year guidance due to COVID-19 uncertainties but provided in-line guidance this time. The Company restated FY 2020 guidance with EPS in the range of $1.42 to $1.59 versus $1.50 consensus analyst estimates and revenue range of $16.50 billion to $16.80 billion analyst estimates. As the economic restarts accelerate, the non-cigarette sales which declined (-9%) should continue to see a recovery in both top line sales and volume. Prudent investors aware of the potential snap back effect of accelerating restarts can look for opportunistic pullback levels to gain exposure Core-Mark shares.

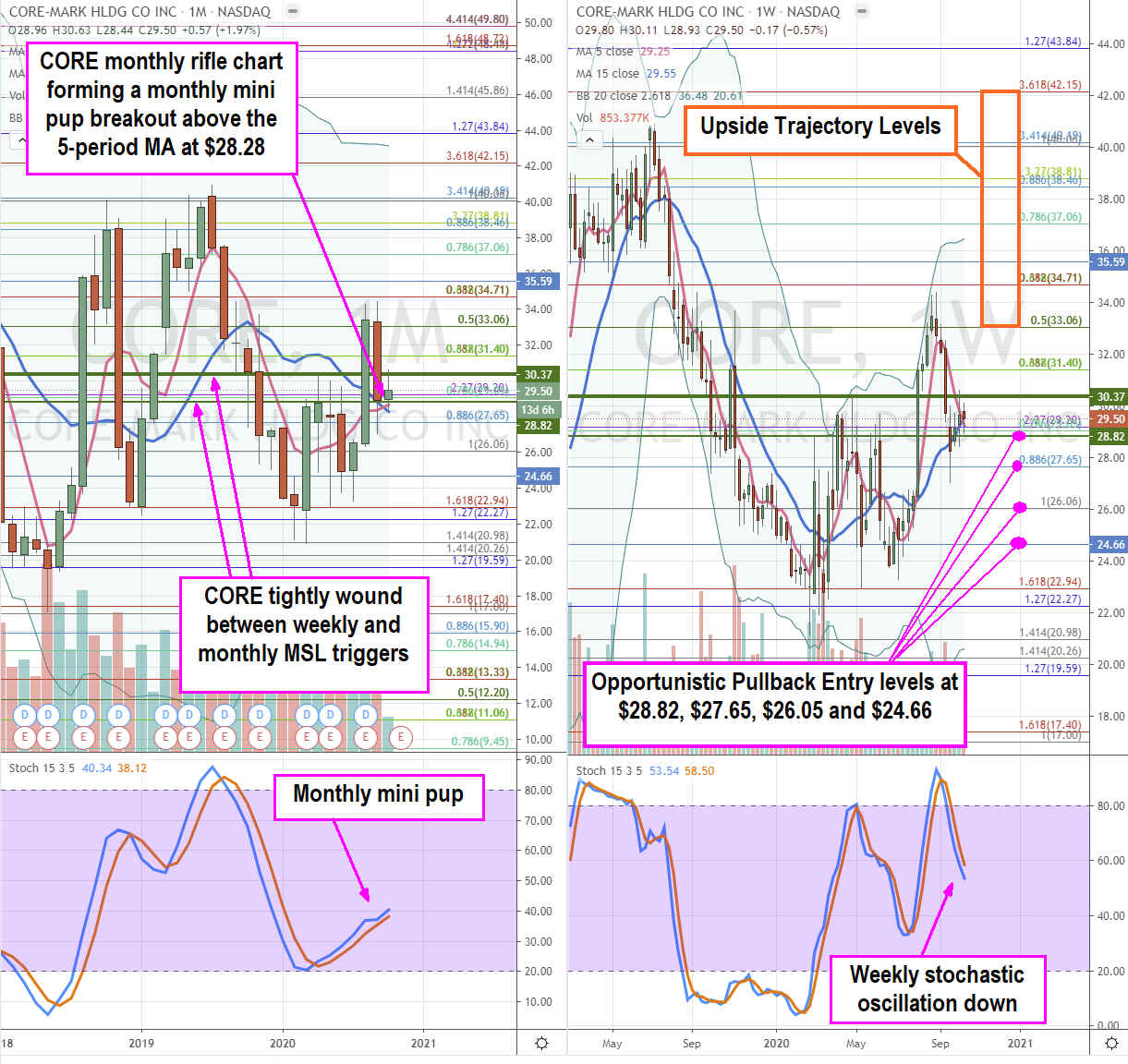

CORE Opportunistic Pullback Levels

Using the rifle charts on the monthly and weekly time frames provides a broader view of the landscape for CORE stock. The monthly rifle chart indicates a new breakout forming with the bullish stochastic mini pup. However, this can be detonate when the weekly stochastic is able to cross back up. Currently the weekly stochastic is still in a down oscillation as the 5-period and 15-period moving averages (MAs) consolidate at the $29.20 Fibonacci (fib) level. The stock is also uniquely wedged between the monthly market structure low (MSL) buy trigger at $30.38 and weekly MSL buy triggers at $28.82. While the weekly stochastic is still slipping, investors can look for opportunistic pullback levels at the $28.32 weekly MSL/fib, $27.65 fib, $26.06 fib and the $24.66 fib. The upside trajectories upon a weekly stochastic cross up triggering the monthly mini pup ranges from the $33.06 fib up towards the $42.15 monthly upper Bollinger Bands (BBs) near the $42.15 fib.