Information and storage management company

Iron Mountain (NYSE: IRM) stock has been floundering below its February pre-COVID highs underperforming the benchmark

S&P 500 index (NYSEARCA: SPY). The world’s largest records and information storage company houses sensitive documents for over 225,000 organizations worldwide including the U.S. government and 95% of the Fortune 1000 on over 90 million square feet of space throughout 50 countries. The Company has been transforming itself to accommodate the digital transformation for enterprises, under the market radar. The market is discounting their data center growth and the ability to leverage existing relationships for digital storage as a one-stop shop for all thing’s storage. The physical records segment hasn’t been affected by the

pandemic while the digital segment is the growth driver. Prudent investors looking to get some exposure can monitor opportunistic pullbacks for exposure.

Q3 FY 2020 Earnings Release

On Nov. 5, 2020, Iron Mountain released its fiscal third-quarter 2020 results for the quarter ending September 2020. The Company reported an adjusted earnings-per-share (EPS) profit of $0.13 excluding non-recurring items versus consensus analyst estimates for $0.14, missing estimates by $0.01. Revenues fell by (2.31%) year-over-year (YOY) to $1.04 billion beating analyst estimates by $42.36 million. The effects of COVID-19 softened the Services revenues which were offset partially from Project Summit benefits and revenue management. Adjusted EBITDA margins expanded 30 to 80 basis points YoY. Project Summit is expected to generate $165 million in benefits for 2020, up from $150 million prior forecast. Total expected adjusted EBITDA benefits are expected around $375 million by end of 2021 with a total cost to implement of $450 million. The Company declared the quarterly cash dividend of $0.62 per share for shareholders on record as of Dec. 15, 2020 and payable on Jan. 6, 2021.

Conference Call Takeaways

Iron Mountain CEO, William Meaney, provided color on the resiliency of its physical storage business and the growing strength of its data centers. The Company saw “gradual improvements” in key U.S. and international markets for its Services segment, which took the worst hit in the quarter. The workforce has 90% of employees back and operating. The Company saw total organic storage rental revenues grow 2.5% from prior quarter crediting emerging markets consumers. Total global organic volume grew two million cubic square feet sequentially. Records management organic volume fell by 1.1 million cubic square feet which is an improvement from the 3.9 million it fell in prior quarter. This is expected to continue fall 1 to 1.5% full year. On the flipside, data center bookings continue to exude strength leasing another 12.3 megawatts (MWs) in the quarter bringing total to 51 MWs. The Company increased its development pipeline for another 50 MWs. Meaney noted that 50% of the development has already been preleased, underscoring the strong backlog.

Hybrid Physical and Digital Information Management

Meaney reiterated the network effect of offering new digital services for legacy storage customers underscoring the hybrid model of information management. New products to help customers with their digital transformation for reliable and secure information management through a hybrid physical and digital storage solutions. This was illustrated with a major U.S. credit union client experiencing 30% YoY growth overwhelming legacy workflows. Iron Mountain improved their mix of paper and digital loan workflows by applying its services from machine learning automation, mailroom services, document scanning and private vault with fire resistance safeguards. Machine learning was applied to automate how the credit union accessed data, verified its accuracy and resolved missing or incorrect items.” This resulted in more than doubling capacity while reducing costs by 25%. As global economic recovery accelerates past COVID-19. Iron Mountain should see its Services segment recover while the data center growth speeds up. Prudent investors can consider scooping up shares of this dividend rich recovery play at opportunistic pullback levels.

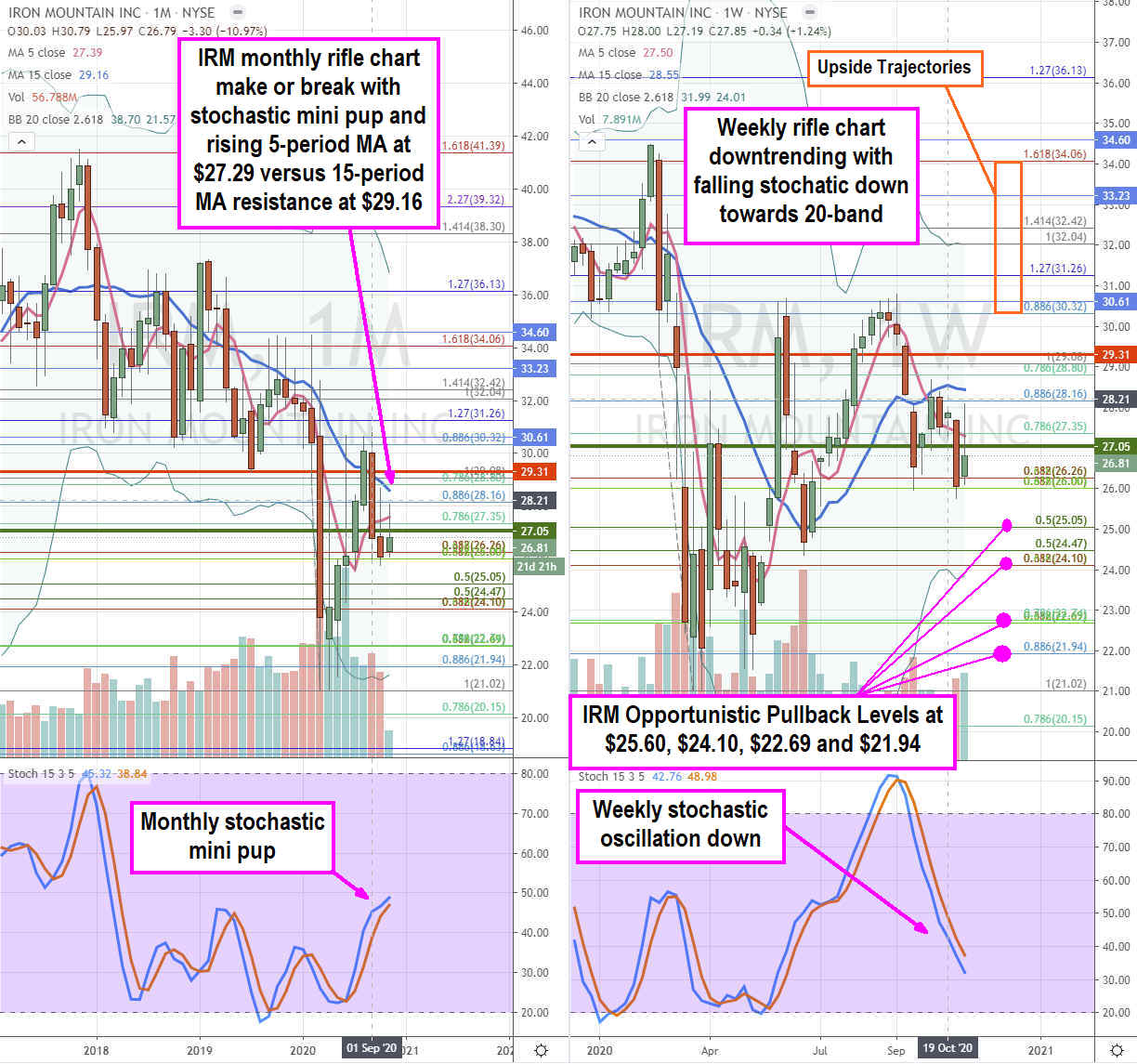

IRM Opportunistic Pullback Levels

Using the rifle charts on the monthly and weekly time frames provides a broader view of the landscape for IRM stock. The monthly rifle chart has make or break set-up with a rising stochastic mini pup but still trading below the monthly 5-period moving average (MA) near the $27.35 Fibonacci (fib) level and 15-period MA at 29.16. This is because of the falling weekly rifle charts which is still in a breakdown with a stochastic oscillation down nearing the 20-band oversold level. The bull case to play out. The weekly The monthly market structure low (MSL) buy triggers above $27.05 for a retest of the monthly 5-period MA and 15-period MA. The weekly stochastic is falling towards the 20-band oversold level. The downdraft can provide opportunistic pullback levels at the $25.05 fib, $24.10 fib, $22.69 fib and the $21.94 fib. Be aware that if the weekly stochastic continues to fall under the 20-band, the monthly stochastic is vulnerable to crossing down and forming an inverse pup breakdown.

Companies in This Article: