PepsiCo (NASDAQ: PEP) released its Q3 2020 earnings yesterday and the report further confirmed that the company’s overall results have not been impacted by COVID, either way. Consider the following two things.

PepsiCo (NASDAQ: PEP) released its Q3 2020 earnings yesterday and the report further confirmed that the company’s overall results have not been impacted by COVID, either way. Consider the following two things.

- Right before the pandemic changed everything, Pepsi expected 4% organic revenue growth for 2020. Well, Pepsi just reinstated its full-year guidance and it still expects 4% organic revenue growth for full-year 2020.

- Pepsi is currently trading right around February 2020 levels.

Yes, earnings are expected to come in a little lower than previously anticipated due largely to COVID-related costs. But its not a huge difference – $5.88 per share vs.$5.50 – and those effects will decrease in 2021.

You may be wondering:

Why has Pepsi been stable when virtually every other company has seen improving or worsening performance? And does an investment in Pepsi make sense moving forward?

Snacks and Beverages Have Offset

Pepsi is comprised of two major businesses – snacks and beverages.

In Q2, Pepsi’s global snack business recorded 5% organic revenue growth, led by Frito-Lay at 7% and Quaker at 23%. But organic revenue growth in global beverages declined by 3%.

In Q3, global snacks increased 6% and global beverages increased 3%.

It’s clear what’s going on here:

When people are stuck at home, they drink less Pepsi, Mountain Dew, Tropicana, etc. They buy those drinks at places like gas stations, restaurants, and bars. With many of those closed or seeing less foot traffic, Pepsi’s beverage sales decline.

On the other hand, people aren’t eating out like they were pre-pandemic, which, as you may have heard, led to pantry loading. While most people now realize the world isn’t going to end, and they’ve stopped cleaning out toilet paper aisles, they are still buying more Frito-Lay and Quaker products than before.

Market Share is Increasing

You may be letting out a yawn at Pepsi’s 2020 performance, but the company’s increasing market share is something to get excited about.

On the Q3 earnings call, CEO Ramon L. Laguarta noted that, “Frito-Lay sustained its strength with 6% organic revenue growth and gained market share in the macro-snack category in the quarter.” Tostitos, already a billion-dollar brand, led the way with double-digit revenue growth.

It has been a similar story in the liquid refreshment category with Laguarta reporting; “Our market share trend within the liquid refreshment beverage category improved versus the previous quarter and we gained market share in the coffee, tea and juice categories.”

No, Pepsi isn’t going to suddenly start running off years of double-digit revenue growth – and maybe not even one year of that – but this company is the definition of slow and steady wins the race.

Attractive Valuation and Yield

PepsiCo investors have only priced modest growth into the shares, as PEP has a forward P/E ratio of 23.7.

The company’s core operating margin declined by 40 basis points in Q3, but if COVID-related costs had been excluded, it would have been an increase of 40 basis points. Long-term margin expansion may certainly be in the cards post-COVID.

Moving to the dividend, while Pepsi isn’t quite a Dividend King, it’s getting there; the company has increased its dividend every year since 1973.

And at nearly 3%, the yield is pretty solid.

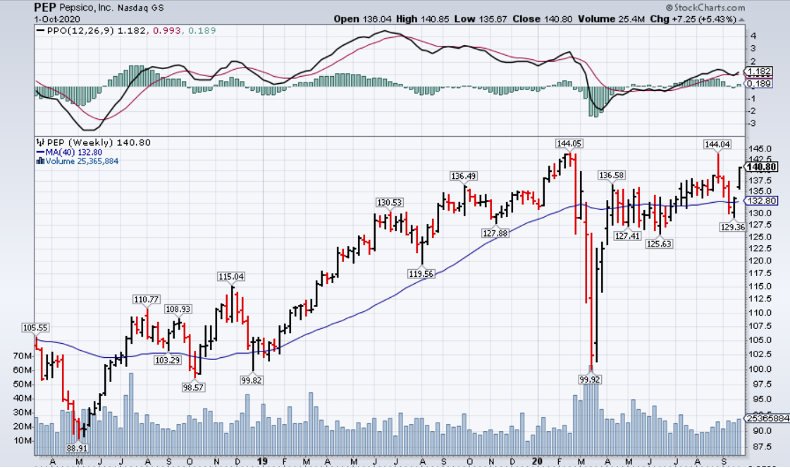

Price Action Has Been Stable

After dropping along with the rest of the market in March – though not as much as most names, I might add – Pepsi quickly recovered. Shares have been bouncing between $125 and $144 over the past six months.

Shares may face some resistance soon, but I think it’s a matter of when – not if – Pepsi will embark on another up-trend.

The Final Word

To answer the second question that I posed in my intro:

Yes, an investment in Pepsi makes sense going forward. It’s not going to make you rich, but it’s going to let you sleep a lot better at night than an investment in, say, Wayfair (NYSE: W).

PEP is a stock you can buy-and-hold for years; you’ll almost definitely get an increasing dividend far into the future and you’ll likely get solid price appreciation as well.

Companies in This Article: